State-Specific Rental Insurance: Pennsylvania Guide

June 13, 2026 · 13 min read

State-Specific Rental Insurance: Pennsylvania Guide

If I run a rental business in Pennsylvania, I usually need more than one policy. At a minimum, I need workers’ comp when I hire my first employee, commercial auto for business vehicles, and my own coverage for rented equipment when it leaves my site.

Here’s the short version: Pennsylvania does not have one single rental-insurance rule that covers every rental type. Instead, I need to line up state law, local rules, lender requests, and my rental contract. I also need to watch a common gap: standard general liability usually does not pay for damage to equipment while a customer has it.

What matters most:

- Workers’ comp is required once I have employees.

- Commercial auto is required for business vehicles and road use.

- General liability often starts at $1 million per occurrence because banks and partners often ask for that limit.

- Inland marine is the policy that usually covers tools, trailers, and equipment off-site.

- Customer COIs help, but they do not replace my own insurance.

- Local rules can change by city or borough. For example, some places may set their own liability minimums.

- [Contactless pickup](https://www.lockii.app/post/contactless-rental-process-planner) adds risk around ID checks, photo records, site safety, and claim proof.

A few Pennsylvania-specific details stand out. The state averages about 42 inches of precipitation per year, which can add slip-and-fall risk at unattended sites. And if I rent out a trailer, coverage may split in two: commercial auto while attached and inland marine once unhitched.

If I want to stay covered, I should keep my asset schedules current, list every location on the policy, check customer COIs before pickup, and use clear digital records for each rental.

Pennsylvania Rental Insurance Basics

How Pennsylvania Defines Rental And Lease Arrangements

Start with the type of asset. In Pennsylvania, rental insurance works one way for property and another way for movable equipment.

Real property rentals cover residential and commercial spaces. Personal property rentals cover movable items like vehicles, trailers, tools, and construction equipment. Those two buckets bring different insurance issues.

With real property, the main risk is premises safety: slip-and-fall claims, fire, and older building systems. With personal property, the focus shifts to off-site use and who has control of the item. That's where the "care, custody, and control" exclusion matters. It means a standard General Liability policy won't pay for physical damage to rented equipment while it's in the customer's hands [1].

Key Insurance Terms Pennsylvania Operators Need To Know

Some insurance terms sound like jargon. But in rental businesses, they directly affect what gets paid and what doesn't.

Care, custody, and control exclusion is one of the biggest trouble spots in rental coverage. Standard General Liability leaves out damage to property in your care, custody, and control. So if your equipment is off-site with a renter, that gap usually needs to be handled by Inland Marine.

Inland Marine coverage, often called a Rental Floater, covers rented assets away from your location. That's a big deal because standard property insurance usually only covers property at your main business address [1].

Replacement Cost vs. Actual Cash Value (ACV) decides how much money comes back after a loss. ACV pays the item's depreciated market value at the time of the loss. Say a trailer costs $14,000 to replace, but depreciation puts its paper value at $8,000. Under ACV, that $8,000 may be all you get. Replacement Cost fills that $6,000 difference [1].

Two other terms show up all the time in rental contracts: Additional Insured and Loss Payee.

- If a renter names you as Additional Insured, their liability policy extends to you.

- If you're listed as Loss Payee, physical damage claim payments go straight to you.

| Term | What It Means For Your Business | | --- | --- | | Care, Custody & Control Exclusion | General Liability won't pay for damage to your equipment while a renter has it | | Inland Marine / Rental Floater | Covers your assets at customer locations, filling the General Liability gap | | Replacement Cost | Pays what it costs to replace the item new, not its depreciated value | | Additional Insured | The renter's liability policy extends coverage to you | | Loss Payee | Physical damage claim payments go directly to you | | Certificate of Insurance (COI) | Proof that the renter's coverage is active and matches your requirements |

These terms also drive the contract rules covered below.

How Pennsylvania Differs From Other States

Pennsylvania stands out in one main way: it leans more on contracts, lender rules, and local requirements than on one statewide rental-insurance statute.

For vehicles and trailers used on the road, commercial auto insurance is required for business use [1]. Commercial auto applies when vehicles and trailers are in transit. Inland Marine steps in once the trailer or equipment is unhitched and sitting at the customer site.

Local governments can add their own rules too. In [Pocono Summit](https://en.wikipedia.org/wiki/Pocono_Summit,_Pennsylvania), for example, short-term rental operators must carry at least $500,000 in liability insurance [3]. So the minimum coverage can change from one Pennsylvania municipality to another.

sbb-itb-eb44693

Mandatory Insurance Requirements For Pennsylvania Rental Businesses

Liability Insurance For Vehicles, Premises, And Operations

Pennsylvania rental requirements come from state law, local ordinances, and contract terms. These are the baseline rules. After that, most operators add more coverage to deal with day-to-day risk.

Commercial auto insurance is legally required for any vehicle your business owns or uses in its operations [1]. Do not rely on a personal auto policy for business driving.

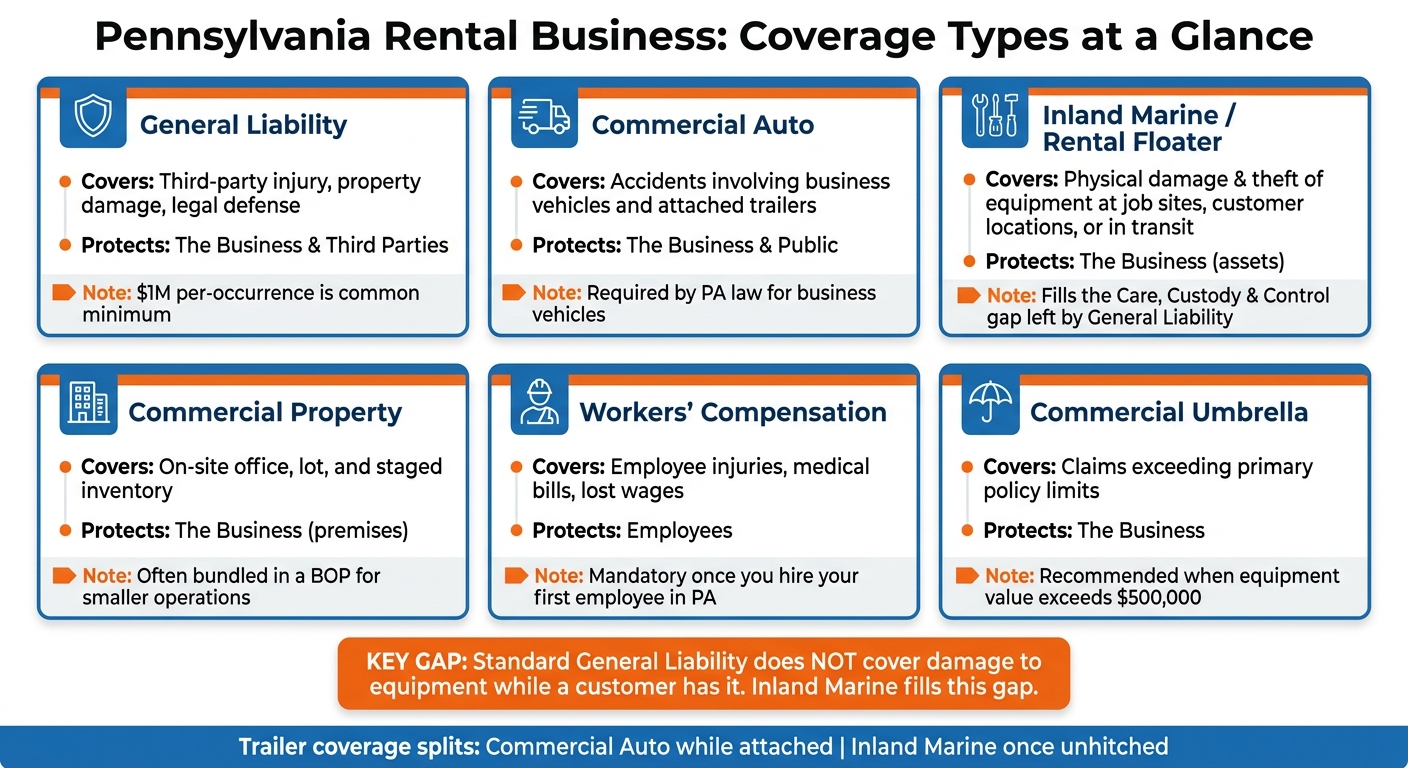

For premises and operations, Commercial General Liability (CGL) is the usual starting point. Many lenders want at least $1 million per occurrence, and standard CGL does not cover damage to property in your care, custody, and control [1].

There’s also an important split with trailers. Commercial auto covers a trailer while it’s attached. Inland marine covers it once it’s unhitched [1]. That matters a lot if you run multiple locations or use contactless pickup.

Workers' compensation becomes mandatory once you hire employees [1].

Insurance Terms Commonly Required In Leases And Rental Contracts

Rental contracts should state insurance duties in plain language. For equipment and trailer rentals, many operators ask customers to provide a current Certificate of Insurance (COI) before pickup. Don’t just collect it and move on. Check that the COI is current and that it matches the limits and coverage type your contract requires [1].

Your contracts should also make a clear distinction between insurance and waivers. A waiver is a contract term, not an insurance policy, so customers should not treat it like a substitute for actual coverage [1]. When those rules are written clearly, it gets much easier to apply the same standard when scaling rental businesses with contactless models.

What Customers Must Cover Vs. What Your Business Must Cover

Your business still needs protection for risks that customer insurance may not fix. That includes theft when the renter’s fault isn’t clear, weather-related loss, equipment transit between renters, and cases where the renter has no insurance or their insurer denies the claim [1].

| Coverage / Requirement | Your Business Should Carry | Customer Role If Required by Contract | | --- | --- | --- | | Third-party liability | CGL | Provide a current COI if your contract requires it | | Physical damage to rental assets | Inland Marine | Customer insurance does not replace this coverage | | Vehicles used in operations | Commercial Auto | Personal auto usually won't cover commercial rental use | | Employee injuries | Workers' Compensation | Not applicable |

Recommended Coverage Types For Rental Fleets And Equipment

Core Business Coverage For Pennsylvania Rental Operators

Once you’ve nailed down customer insurance rules, the next step is protecting your rental business.

For many Pennsylvania rental operators, the starting point is Commercial General Liability (CGL). This policy helps cover third-party bodily injury and property damage claims tied to your lot or day-to-day operations. A $1 million per-occurrence limit is a common starting line [1].

You’ll also want Commercial Property coverage for your office, lot, and staged inventory waiting to go out. If you run a smaller operation, you can often combine CGL and Commercial Property in a Business Owner's Policy (BOP) to save money. That said, a BOP usually leaves out auto and inland marine coverage, so it doesn’t cover the whole setup [1].

A Commercial Umbrella policy starts to make sense once your equipment value climbs past $500,000. It sits on top of your main policies and helps pay claims that go past those limits [1].

Fleet, Trailer, And Equipment Coverage

When you’re insuring mobile assets, it helps to think in plain terms: is the item attached, detached, or sitting at a customer site?

Commercial auto usually covers attached trailers. Inland Marine steps in for detached equipment at customer sites, job sites, and while it’s in transit.

Inland Marine covers movable equipment against theft, fire, vandalism, and accidental damage at customer locations, job sites, or in transit [1]. And when you set that policy up, choose replacement cost instead of actual cash value (ACV). If you go with ACV, depreciation can leave you paying part of the replacement bill yourself [1].

| Coverage Type | What It Covers | Who It Protects | | --- | --- | --- | | General Liability | Third-party injury, property damage, and legal defense | The Business / Third Parties | | Commercial Auto | Accidents involving business vehicles and attached trailers | The Business / Public | | Inland Marine | Physical damage/theft of equipment at job sites or in transit | The Business (assets) | | Commercial Property | On-site office, lot, and staged inventory | The Business (premises) | | Workers' Comp | Employee injuries, medical bills, and lost wages | Employees | | Umbrella Policy | Claims exceeding primary policy limits | The Business |

Customer Protection Options And Pennsylvania Cost Context

Asking renters to carry their own insurance can help protect your loss history. But it does not replace your own commercial coverage. Each Certificate of Insurance (COI) should be current, match the planned use, and carry limits that fit the asset value or rental type involved [1].

Pricing will depend on your fleet size, total asset value, and claims history, which is why it helps to work with a broker who knows rental operations [1]. You’ll also want to make sure the care, custody, and control exclusion is handled the right way, along with any gap between auto and inland marine coverage [1].

These choices get tougher as your operation grows. Add more locations or contactless pickup, and one weak spot in coverage can affect multiple branches at once, especially when solving labour shortages through automation.

Multi-Location And Contactless Rentals In Pennsylvania

How Multiple Pennsylvania Locations Affect Coverage And Risk

Once your core policies are set, every new site adds another layer of compliance risk. Each lot, yard, and pickup point needs to be listed on the policy that covers it. If a site isn't listed, a carrier can deny a claim [1].

Where a site sits also changes both risk and price. Urban locations like Philadelphia and Pittsburgh usually come with more liability exposure and higher repair or replacement costs. Dense traffic, older infrastructure, and higher litigation rates all play a part. Rural and resort markets have a different set of problems, with more weather exposure and harder-to-manage remote sites [2]. On top of that, local minimums can change by municipality, so policy limits should line up with each site's rules.

| Location Type | Primary Risk Factors | Insurance Implications | | --- | --- | --- | | Urban (e.g., Philadelphia) | High traffic, theft exposure, aging infrastructure | Higher liability premiums; higher replacement cost valuations [2] | | Suburban (e.g., Lehigh Valley) | Mixed traffic, moderate weather, shared lots | Standard commercial rates; premises liability focus [2] | | Rural/Mountain (e.g., Poconos) | Severe winter weather, remote locations, nor'easters | Higher Inland Marine needs; specific local liability minimums [3] |

Some Pennsylvania municipalities also require a designated local contact who can be reached 24/7 when the owner or main operator is more than 20 miles from the site [3]. If you're growing across the state, that can't sit on a back burner. It needs to be built into daily operations.

That pressure gets even higher when you move to unattended pickup.

Contactless Pickup Risks And Required Controls

A 24/7 self-service model removes the in-person handoff. And that means several checkpoints insurers often look for during a claim review are gone too. If you don't replace that process with securing contactless rentals through clear, recorded procedures, the weak spots stack up fast.

The main trouble areas are identity fraud, premises liability, and claim evidence. With contactless access, it's easier for someone to book with false details and leave with your equipment. Then there's the site itself. Pennsylvania averages 42 inches of annual precipitation, which adds ice, snow, and slip-and-fall risk at unattended lots [2]. And if damage shows up later, proving whether it happened before or after the rental gets much harder without staff on site and a clean digital record.

The care, custody, and control gap still applies, which means GL does not cover damage to rental inventory.

Insurers usually want documented controls, not loose habits. That often includes:

- Identity verification before access is granted

- Digital agreement acceptance

- Condition photos at pickup and return

- A clear audit trail for each booking [1]

Those records can make a claim much easier to defend when something goes sideways.

For trailers, the split between commercial auto and inland marine can also get messier once pickup is unattended.

Whatever controls you use, they need to be documented and repeatable across every site.

Using Lockii To Support Insurance Compliance Workflows

Lockii is built for contactless, multi-location rental operations. It can centralize identity verification, digital access, hire-end photos, audit logs, GPS tracking, SMS and email notices, and maintenance records across every site. For unattended operations, that paper trail can support insurance compliance and help defend claims.

Pennsylvania Rental Insurance Compliance Checklist

Use this checklist to keep coverage, contracts, and records lined up as your business grows.

Set Up A Pennsylvania-Compliant Insurance Program

Make sure your required policies are active, set up the right way, and tied to the right assets.

- Keep the Inland Marine schedule current each time you add equipment or open a new location.

- Check that your Commercial Auto policy includes every vehicle used for business operations or delivery.

- For trailers, make sure Inland Marine also covers the unit while it's unhitched at a customer's site. That's the gap that often leaves equipment uninsured while parked [1].

- Match liability limits to local minimums, and insure equipment at replacement cost [1].

After that, tighten up your contract language so every location follows the same insurance rules.

Standardize Contracts And Customer Insurance Rules

Every rental contract across your Pennsylvania locations should use the same language on damage responsibility and banned uses. If one location says one thing and another booking channel says something else, claims can get messy fast.

Spell out in the contract who handles damage, what uses are allowed, and what insurance is required. If you collect a Certificate of Insurance (COI) from a customer, check the COI limits, coverage type, and expiration date before pickup [1]. Build COI review into the booking workflow instead of leaving it until the last minute.

Review these rules on a set basis, especially after opening a new location or changing how pickups work.

Monitor, Audit, And Update Coverage As You Scale

Review coverage any time locations, assets, or pickup methods change. New assets should be scheduled before they leave the lot, not after a claim shows up.

The table below lays out the main compliance tasks, who should handle them, and how to document each one:

| Task | Responsible Role | Review Frequency | Proof / Documentation Method | | --- | --- | --- | --- | | Asset Schedule Audit | Fleet Manager | Monthly / Upon Acquisition | Updated Inland Marine Policy Schedule | | COI Verification | Rental Agent | Per Booking | Digital copy of COI with verified expiration date [1] | | Commercial Auto Compliance Check | Owner | Annual | Valid Commercial Auto ID cards for all road-use assets [1] | | Municipal Permit Review | Compliance Officer | Annual | Valid City/Borough Rental License or Permit (e.g., Philadelphia, Pittsburgh) [3] | | Workers' Comp Audit | HR / Owner | Annual | Certificate of Workers' Compensation Insurance [1] | | Inland Marine Review | Risk Manager | Twice yearly | Policy endorsement confirming coverage for unattached/unattended assets | | Digital Log Review | Operations Manager | Weekly | Lockii access logs and digital contract records |

For contactless and multi-location operations, Lockii's audit logs, digital contracts, and GPS tracking help keep records in one place across every site. Philadelphia requires rental records to be kept for at least one year [3], so a central digital system is much easier to run.